Just a quick version of where things stand as of this writing: President Trump has targeted $50 billion worth of Chinese imports with 10% tariffs. China is threatening retaliatory tariffs of their own on goods we export to that country. If China does indeed retaliate, the President has now threatened tariffs on $200 billion in Chinese imports -- four times the initial target.

Whether this turns into a full-blown trade war or not is anyone��s guess at this point. However, there are some clear disadvantages to a trade war that Americans should be aware of.

ALSO READ: What Stocks Perform Well in the Midst of a Trade War?

Man opens wallet and dollar bills fly out. (Photo: Getty Images)

Costs of everyday products could increase

A trade war could impact Americans�� wallets in several ways, including higher prices on items we buy every day. Specifically, tariffs on imported materials are likely to be passed on to consumers.

In some ways this could be minimal. If a food manufacturer uses a small amount of, say, imported aluminum to make their packaging, the additional cost to you is likely to be negligible. However, there could be large increases on some products�� prices.

For example, let��s say that an appliance manufacturer uses $100 worth of imported steel when making a product. If there��s a 25% tariff added to the steel, the manufacturer��s cost will increase by $25, which is likely to be passed on to the consumer in the form of higher prices.

From China specifically, we import quite a bit of electronics, toys, and clothing, just to name a few categories, so you may notice these things start to cost more if tariffs go into effect.

Interest rates on pieces of cut out paper. (Photo: Getty Images)

Inflation could lead to even higher interest rates

When the costs of goods and services rise, we call that�inflation. As of June 2018, inflation is running right about 2% per year -- right where the Federal Reserve wants it.

If inflation picks up because of higher costs to consumers, the Federal Reserve is likely to raise interest rates even faster than it currently plans to do. The Fed already plans to do about eight more quarter-percent rate hikes by the end of 2020 based on its�current inflation projections, which aren��t much higher than its 2% target.

This could make the cost of borrowing money higher for all U.S. consumers, as bank lending rates tend to move in the same direction as Federal Reserve interest rate activity.

A pile of four different credit cards. (Photo: Getty Images)

Credit card interest rates could see a spike

One of the most direct effects of Federal Reserve interest rate hikes is higher credit card APRs. Credit card interest rates are generally derived from the Prime Rate, which is directly linked to the Federal Funds Rate -- the interest rate the Federal Reserve moves up and down.

Let��s say that you have a credit card that currently has a 16.99% APR. Based on the Fed��s current projections of eight 25-basis-point rate hikes by the end of 2020, you can expect your APR to gradually rise to 18.99% over the next couple of years. However, if the Fed gets more aggressive with its rate hikes because of inflation, your APR could easily get significantly higher.

ALSO READ: These 3 Companies Could Be Huge Trade War Casualties

Man in suit holds his head while looking at plunging line graphs. (Photo: Getty Images)

Economic activity could drop

The economy has been firing on all cylinders, but that could come to a screeching halt if a trade war escalates.

In April, the Tax Foundation determined that the proposed tariffs on high-tech Chinese imports would lower GDP and wage growth by 0.1%. What��s more, it would cost the U.S. 79,000 jobs. And keep in mind that this is just one type of proposed tariff. The effects of a full-blown trade war could be much more severe.

Furthermore, the Brookings Institution estimates that as many as 2.1 million U.S. jobs could be affected by China��s initial retaliatory tariffs alone. The University of Pennsylvania said that an all-out trade war would reduce U.S. GDP by 0.9% by 2027, and wages by 1.1%.

In a nutshell, a trade war could be bad news for the U.S. economy and could derail our growth trajectory.

Stock quotes page of newspaper. (Photo: Getty Images)

Stocks could take a hit

Higher interest rates, higher costs of goods and services, and reduced economic activity are not positive catalysts for the stock market. Higher interest rates generally lead to lower consumer spending, and the same can be said for higher prices.

So, if an all-out trade war breaks out, you can expect it to put negative pressure on stocks. Income-focused stocks, such as REITs and other high-dividend stocks, are especially vulnerable to rising rates, although all stocks could feel the squeeze from generally lower economic activity.

Couple looking at bills with hands over their mouths. (Photo: Getty Images)

Not good for consumers or investors

The bottom line is that a trade war could make life more expensive and could make your investments lose value.

To be perfectly clear, we��re not in an all-out trade war with China (or anyone else) just yet, but it certainly appears that we��re getting closer by the day. And, it��s important to know what to expect if it happens.

The Motley Fool has a�disclosure policy.The Motley Fool is a USA TODAY content partner offering financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

Offer from the Motley Fool:�10 stocks we like better than BlackLine, Inc.

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade,�Motley Fool Stock Advisor, has quadrupled the market.*

David and Tom just revealed what they believe are the�10 best stocks�for investors to buy right now... and BlackLine, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here�to learn about these picks!

*Stock Advisor returns as of June 4, 2018

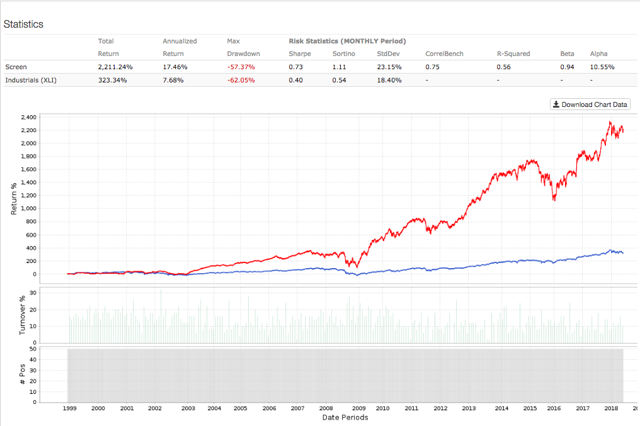

Data from S&P Global via Portfolio123

Data from S&P Global via Portfolio123 Vision Capital Management Inc. purchased a new stake in shares of iShares Russell 2000 Index (NYSEARCA:IWM) in the 2nd quarter, according to the company in its most recent 13F filing with the SEC. The firm purchased 1,266 shares of the exchange traded fund’s stock, valued at approximately $207,000.

Vision Capital Management Inc. purchased a new stake in shares of iShares Russell 2000 Index (NYSEARCA:IWM) in the 2nd quarter, according to the company in its most recent 13F filing with the SEC. The firm purchased 1,266 shares of the exchange traded fund’s stock, valued at approximately $207,000.  Xact Kapitalforvaltning AB raised its stake in Gilead Sciences, Inc. (NASDAQ:GILD) by 4.7% during the first quarter, according to its most recent disclosure with the Securities and Exchange Commission (SEC). The fund owned 261,826 shares of the biopharmaceutical company’s stock after buying an additional 11,835 shares during the quarter. Xact Kapitalforvaltning AB’s holdings in Gilead Sciences were worth $19,739,000 at the end of the most recent quarter.

Xact Kapitalforvaltning AB raised its stake in Gilead Sciences, Inc. (NASDAQ:GILD) by 4.7% during the first quarter, according to its most recent disclosure with the Securities and Exchange Commission (SEC). The fund owned 261,826 shares of the biopharmaceutical company’s stock after buying an additional 11,835 shares during the quarter. Xact Kapitalforvaltning AB’s holdings in Gilead Sciences were worth $19,739,000 at the end of the most recent quarter.